From left to right:

John Waldron

David Solomon

Denis Coleman

From left to right:

John Waldron

David Solomon

Denis Coleman

Twenty twenty-three was a year of execution for Goldman Sachs. We took swift, decisive action to refocus the firm’s strategy while at the same time strengthening our core businesses, and I’m proud of the progress we made. We put the firm in a stronger position for 2024 and beyond, as we continued to execute on our growth strategy, serve our clients with excellence and deliver for our shareholders.

As we enter 2024, our strategy is centered on our two core businesses, where we have proven our “right to win” with our leadership positions, scale and exceptional talent, and as CEO, I am focused on our three strategic objectives:

- Harness One Goldman Sachs to serve our clients with excellence.

- Run world-class, differentiated and durable businesses.

- Invest to operate at scale.

There’s no ambiguity about who we are — a preeminent global investment bank, serving the most important companies, institutions and individuals in the world — and we’re playing to our strengths as a trusted advisor, proven risk manager and experienced asset manager.

One reason I’m excited about the future is the strength of our core franchise. We have two world-class and interconnected businesses: Global Banking & Markets, which comprises our top-ranked investment bank1 as well as FICC and Equities, and Asset & Wealth Management, a leading global active asset manager with a top 5 alternatives business2 and a premier ultra–high net worth wealth management franchise.

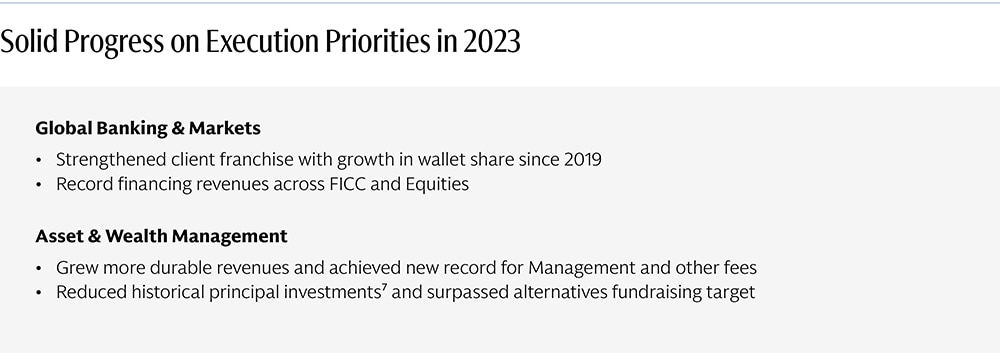

Over the past year, we have continued to enhance our franchise. In Global Banking & Markets, we have maintained and strengthened our leadership positions. We were #1 in Advisory net revenues for the 21st year in a row as well as #1 in equity and equity-related underwriting volumes and #2 in high-yield debt volumes.3 We were also #1 in Equities and a top 3 player in FICC,4 where we achieved our second-highest net revenue year since 2010.

It’s clear that our One Goldman Sachs operating ethos and client-centric approach are having an impact. In Global Banking & Markets, we have increased our wallet share by nearly 350 basis points since 2019,5 and in FICC and Equities, we are in the top 3 with 117 of the top 150 clients — up from 77 in 2019.6 In addition, since 2019, our financing revenues across FICC and Equities have grown at a 15 percent compounded annual growth rate to a record of nearly $8 billion in 2023.

In Asset & Wealth Management, we have continued to grow our more durable revenue base. Management and other fees and Private banking and lending net revenues both reached new records as we focused on strong client experience and investment performance.

I am also proud to report that, since 2019, we have raised over $250 billion in alternatives, surpassing our $225 billion target a year early. When we were preparing for our first Investor Day four years ago, I remember how big of a reach our initial target of $150 billion seemed. To surpass both our original and our higher, revised target one year ahead of schedule demonstrates the power of our platform.

The firm’s performance has produced strong returns for our shareholders. Over the past five years, book value per share has grown by approximately 50 percent, our stock price has risen by approximately 130 percent (compared to a peer average of approximately 60 percent) and our quarterly dividend has more than tripled.

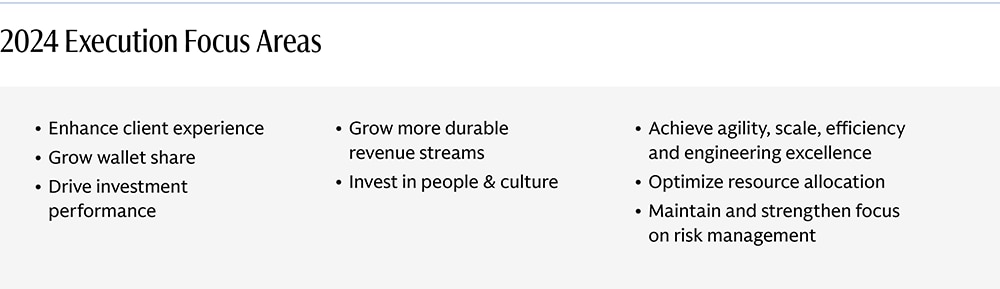

For 2024, we’re focused on our execution priorities, which are highlighted in the table below. We believe our strategic objectives and these focus areas will help us achieve our desired outcomes:

- To continue to be a trusted advisor to our clients;

- To be an employer of choice for our people; and

- To generate mid-teens returns through the cycle and strong shareholder return.

I am now hearing consistently that our strategy has never been clearer, and I’m proud to say that’s a direct result of everything we achieved in 2023.

Another reason I’m optimistic about 2024 is that the firm stands to benefit as capital markets rebound. Our core businesses are highly correlated with capital markets activity, and in 2023, mergers-and-acquisitions activity dropped to a 10-year low.

After years of easy monetary policy and fiscal stimulus, economic conditions tightened at the fastest rate in 40 years, and yet there was not a recession. The U.S. economy has proven more resilient than expected, and markets are predicting rate cuts, though I think inflation may prove stickier than many anticipate. Either way, the cost of capital is now materially higher, and markets are adjusting.

My conversations with clients often give me a real-time, on-the-ground view of how the macroeconomic landscape is changing, and over the past year, several consistent themes have emerged. Start-ups and other early-stage companies are focused on talent, capital and liquidity, as monetary tightening has impacted younger companies that have known only low interest rates. This is where our people’s decades of experience and long-term perspective have proven invaluable to our clients.

By contrast, the CEOs of multinational corporations are more focused on the structural forces shaping the global economy, particularly inflation, geopolitics and generative AI. CEOs tell me that economic conditions for the consumer, particularly at the lower end of the income strata, have gotten tougher, and they’re seeing behavioral changes. But the Fed now has room to ease if economic conditions start to decline.

There’s no question that generative AI is going to disrupt a wide range of industries. But I believe it’s important to keep perspective. Some predict that AI code generation tools could increase developer productivity from 20 to 45 percent,9 and the pace of change in research and development is increasing at a remarkable rate. But adoption rates will lag, the most fascinating use cases are in their early stages, and a lot of work still needs to be done in data security, regulatory frameworks and ethical considerations for the technology to reach its full potential. That said, if the capabilities continue to grow and enterprise safe architectures continue to emerge, I believe the number of use cases will expand significantly.

Never far from our minds is geopolitics, particularly the three flashpoints of Ukraine, the Middle East and China. Looking at China specifically, CEOs are debating whether and how to shift their supply chains, though China’s economy and the U.S.’s will continue to be significantly intertwined. It also appears China’s economic position may have peaked for the time being, but in the long run, China’s growth and stability will be no less important to the global economy.

Regulatory Landscape

Clients and investors are also concerned about the regulatory environment.

One effort in particular has come under scrutiny. In 2023, U.S. regulators unveiled a proposal to raise capital requirements for large banks known as Basel III reforms. We believe strongly in preserving and enhancing the safety and soundness of the financial system, but in our view the proposal would hurt economic activity without improving financial stability. It would also result in several unintended consequences.

First, we believe the cost of credit would go up for many of our clients, ranging from manufacturers to energy companies to retirement savers, and they would likely pass on those higher costs to consumers. For example, we would need to hold in reserve substantially more capital for common transactions we make with pension funds that improve their returns for retirees.

Second, we believe the proposal would hurt U.S. competitiveness. U.S. regulators did not provide many of the same flexibilities that European regulators did for their banks. As a result, U.S. banks will be less able to provide credit and liquidity to clients, and costs will rise.

Third, we believe the proposal would drive credit and lending activity out of the regulated banking sector and into unregulated parts of the economy. Because regulators have far less visibility into these sectors, we could see a buildup of risks that could ultimately lead to financial shocks. In addition, regulators have found that these so-called shadow banks can pull back significantly during periods of stress, which further decreases market liquidity.

We have been active in advocating for major revisions to the proposal, and we are not alone. According to public analysis, over 97 percent of comment letters expressed substantial concerns with at least one important aspect of the proposal.10 Many public and private companies, pension funds, and investing institutions argued it would reduce access to credit, make it harder to manage risks and harm capital markets.

A sound and safe financial system is critical to the functioning of the U.S. economy, but we believe this proposal does not adequately serve the interests of the broader public and must be revised.

In 2023, we made a significant commitment to reinvest in one of our biggest competitive advantages: our culture.

Built upon our core values of partnership, client service, integrity and excellence, our culture is what defines us, it is our identity and it is at the heart of our commercial success.

In the aftermath of the pandemic and the further strains of a changing world, we launched the Cultural Stewardship Program to reinforce our individual and collective responsibility to protect and enhance our culture. Between late 2022 and early 2024, I met with almost all of our partners in 19 sessions, where we discussed what makes our culture special.

There was widespread agreement that ours is a collaborative culture, and by “collaborative” I don’t mean simply that we work together in an appropriate manner, but also that we provide mutual support in achieving shared goals and outcomes. Our culture emphasizes teamwork, trust and respect for others’ perspectives and expertise. Most of all, it encourages the free flow of ideas and the sharing of knowledge. In the process, we create a feeling of belonging.

We are also a culture of apprenticeship. We teach our colleagues who are just starting out in their careers how to conduct our business and how to engage with clients. But more importantly, each of us has an obligation to pass down the values that define what it means to be a Goldman Sachs professional. And that comes through our demonstrated actions: how we handle ourselves in difficult moments, our thought process, and our ability to resist short-term thinking in order to maximize the client’s and the firm’s long-term interests.

Throughout the firm, our people are passionate about our culture and understand we must continue to invest in it. After all, our culture fuels our success; we can never take it for granted.

In the year ahead, our focus is on strengthening the firm by providing world-class solutions for our clients as well as investing in our culture and our people. I’m confident that, if we continue to serve our clients well, we will build on last year’s progress and position the firm to deliver strong returns for shareholders. The changing environment and our streamlined strategy are ushering in a new chapter for the firm. When I think about the strength of our market position, the depth and breadth of our client franchise, and the caliber of our people, I couldn’t be more excited about the future of Goldman Sachs.

David Solomon

Chairman and Chief Executive Officer

We aspire to be the world’s most exceptional financial institution, united by our shared values of partnership, client service, integrity and excellence.

We distilled our Business Principles into four core values that inform everything we do:

Partnership | Client Service | Integrity | Excellence

Our clients’ interests always come first.

Our experience shows that if we serve our clients well, our own success will follow.

Our assets are our people, capital and reputation.

If any of these is ever diminished, the last is the most difficult to restore. We are dedicated to complying fully with the letter and spirit of the laws, rules and ethical principles that govern us. Our continued success depends upon unswerving adherence to this standard.

Our goal is to provide superior returns to our shareholders.

Profitability is critical to achieving superior returns, building our capital, and attracting and keeping our best people. Significant employee stock ownership aligns the interests of our employees and our shareholders.

We take great pride in the professional quality of our work.

We have an uncompromising determination to achieve excellence in everything we undertake. Though we may be involved in a wide variety and heavy volume of activity, we would, if it came to a choice, rather be best than biggest.

We stress creativity and imagination in everything we do.

While recognizing that the old way may still be the best way, we constantly strive to find a better solution to a client’s problems. We pride ourselves on having pioneered many of the practices and techniques that have become standard in the industry.

We make an unusual effort to identify and recruit the very best person for every job.

Although our activities are measured in billions of dollars, we select our people one by one. In a service business, we know that without the best people, we cannot be the best firm.

We offer our people the opportunity to move ahead more rapidly than is possible at most other places.

Advancement depends on merit and we have yet to find the limits to the responsibility our best people are able to assume. For us to be successful, our people must reflect the diversity of the communities and cultures in which we operate. That means we must attract, retain and motivate people from many backgrounds and perspectives. Being diverse is not optional; it is what we must be.

We stress teamwork in everything we do.

While individual creativity is always encouraged, we have found that team effort often produces the best results. We have no room for those who put their personal interests ahead of the interests of the firm and its clients.

The dedication of our people to the firm and the intense effort they give their jobs are greater than one finds in most other organizations.

We think that this is an important part of our success.

We consider our size an asset that we try hard to preserve.

We want to be big enough to undertake the largest project that any of our clients could contemplate, yet small enough to maintain the loyalty, the intimacy and the esprit de corps that we all treasure and that contribute greatly to our success.

We constantly strive to anticipate the rapidly changing needs of our clients and to develop new services to meet those needs.

We know that the world of finance will not stand still and that complacency can lead to extinction.

We regularly receive confidential information as part of our normal client relationships.

To breach a confidence or to use confidential information improperly or carelessly would be unthinkable.

Our business is highly competitive, and we aggressively seek to expand our client relationships.

However, we must always be fair competitors and must never denigrate other firms.

Integrity and honesty are at the heart of our business.

We expect our people to maintain high ethical standards in everything they do, both in their work for the firm and in their personal lives.

Forward-Looking Statements

This letter contains forward-looking statements, including statements about our financial targets, business initiatives, capital markets and M&A activity levels, the impact of AI on productivity, the potential impact of changes to U.S. regulatory capital rules, and interest rate and inflation trends. You should read the cautionary notes on forward-looking statements in our Form 10-K for the period ended December 31, 2023. For information about some of the risks and important factors that could affect the firm’s future results and the forward-looking statements, see “Risk Factors” in Part I, Item 1A of the firm’s Annual Report on Form 10-K for the year ended December 31, 2023.

1Based on cumulative publicly disclosed Investment Banking revenues from 2020 to 2023. Peers include MS, JPM, BAC, C, BARC, DB, UBS, CS (through 2022).

2Rankings as of 4Q23. Peer data compiled from publicly available company filings, earnings releases and supplements, and websites, as well as eVestment databases and Morningstar Direct. GS total Alternatives investments of $485 billion as of 4Q23 includes $295 billion of Alternatives assets under supervision (AUS) and $190 billion of non-fee-earning Alternatives assets.

3Ranking for Advisory net revenues based on reported revenues (2003–2023). Ranking for equity and equity-related and high-yield debt underwriting volumes are per Dealogic (January 1, 2023, through December 31, 2023).

4Ranking for Advisory net revenues based on reported revenues (2003–2023). Ranking for equity and equity-related and high-yield debt underwriting volumes are per Dealogic (January 1, 2023, through December 31, 2023).

5Revenue wallet share since Investor Day 2020 (2023 vs. 2019). Based on reported revenues for Advisory, Equity underwriting, Debt underwriting, FICC and Equities. Total wallet includes GS, MS, JPM, BAC, C, BARC, DB, UBS, CS (through 2022).

6Source: Top 150 client list and rankings compiled by GS through Client Ranking / Scorecard / Feedback and / or Coalition Greenwich 1H23 and FY19 Institutional Client Analytics ranking.

7Historical principal investments include consolidated investment entities and other legacy investments the firm intends to exit over the medium term (medium term refers to a 3–5-year time horizon from year-end 2022).

8Five-year stock price return as of December 31, 2023. Peers include MS, JPM, BAC, C.

9McKinsey & Company. “The economic potential of generative AI: The next productivity frontier.” June 14, 2023.

10Latham & Watkins, LLP. “The Basel III Endgame Proposal: Public Comments Snapshots.” February 2, 2024.