Goldman Sachs Research expects the global economy to outperform expectations in 2024 — just as it did in 2023.

That outlook is based on our economists’ prediction for strong income growth (amid cooling inflation and a robust job market), their expectation that rate hikes have already delivered their biggest hits to GDP growth, and their view that manufacturing will recover. Central banks, meanwhile, will have room to reduce interest rates if they’re concerned about the economy slowing. “This is an important insurance policy against a recession,” Goldman Sachs Research Chief Economist Jan Hatzius writes in the team’s report titled Macro Outlook 2024: The Hard Part Is Over.

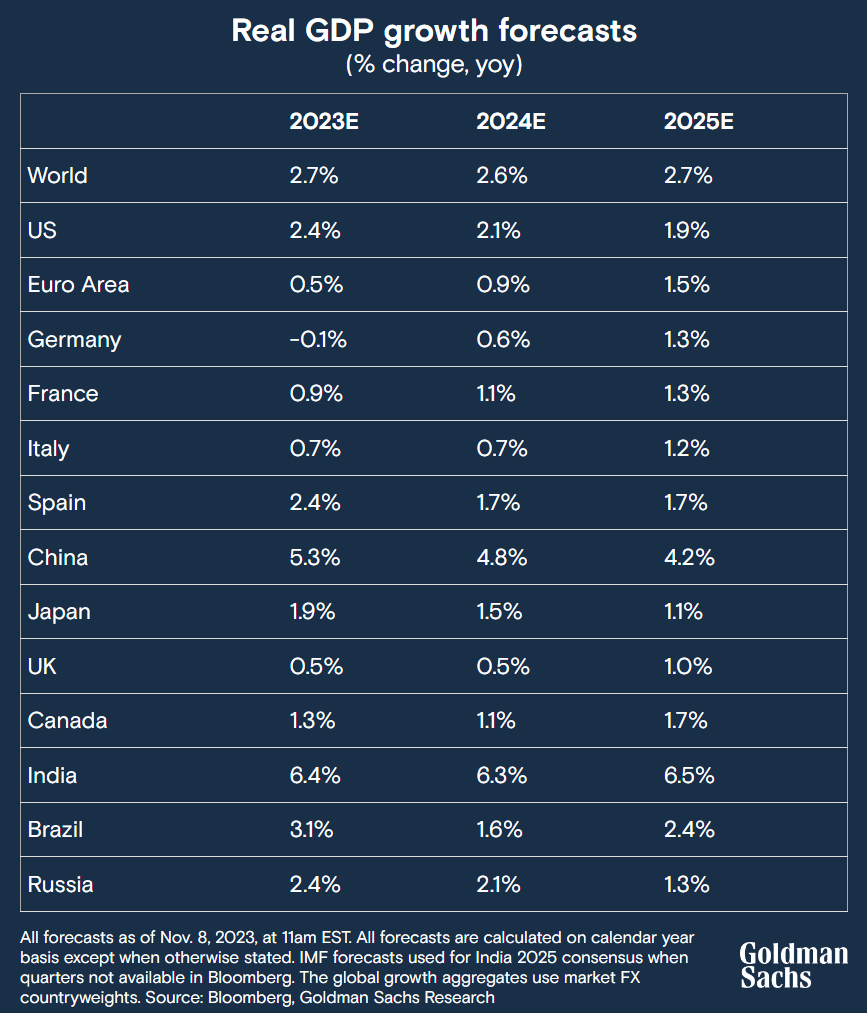

Worldwide GDP is forecast to expand 2.6% next year on an annual average basis, compared with the 2.1% consensus forecast of economists surveyed by Bloomberg. In fact, Goldman Sachs Research’s forecasts for GDP growth in 2024 are more optimistic than the consensus for eight of the world’s nine largest economies, as of Nov. 8, 2023. And notably, our economists expect US growth to outpace its developed market peers again.

The global economy fared better than many economists expected in 2023

Goldman Sachs Research was also optimistic about the global economy in 2023 — and the results have exceeded even our own economists’ expectations.

Solid GDP growth has translated into more-than-solid labor market performance. The unemployment rate across all the economies covered by our analysts (and with high-quality labor market data) now stands about 0.5 percentage points below its pre-pandemic level. Importantly, this improvement is visible even in some key economies that have seen very low real GDP growth, such as the Euro area.

Will inflation continue to cool in 2024?

Importantly, GDP growth and employment have been surprisingly buoyant among economies that experienced a large and unwanted inflation surge in 2021-2022. (Policymakers in Japan, by contrast, wanted inflation.) And inflation is now cooling across G10 and emerging market economies.

“We don’t think the last mile of disinflation will be particularly hard,” Hatzius writes. The supply and demand of goods have grown more balanced, and the impact of this on core goods disinflation is still unfolding and is forecast to continue through most of 2024. Shelter inflation is expected to have considerably further to fall.

Most crucially, the supply-demand balance in the labor market continues to improve. Goldman Sachs Research’s jobs-workers gap — measured as job openings minus unemployed workers — is trending down everywhere. The adjustment has so far occurred almost entirely in a benign fashion, as job openings have declined without a rise in unemployment.

Our economists forecast this year’s decline in inflation to continue in 2024: sequential core inflation is predicted to fall from 3% now to an average 2-2.5% range across the G10 (excluding Japan). “That would be broadly consistent with the inflation targets of most developed market central banks by the end of 2024,” Hatzius writes. “If anything, we think that the risks to the achievement of target-consistent inflation are on the earlier side.”

Many big economies will avoid recession in 2024

Over the past year, our economists have been relatively optimistic that major economies can avoid a recession. In the team’s report, they reaffirm their longstanding view that the probability of a US recession is much lower than commonly appreciated — at just 15% over the next 12 months.

There are four main reasons Goldman Sachs Research is optimistic about growth next year.

- Our economists have a positive outlook for real disposable income growth at a time of much lower headline inflation and still-strong labor markets. While they predict US real income growth will slow from its very strong 2023 pace, they think it will still be enough to support consumption and GDP growth of at least 2%. Meanwhile, both the Euro area and the UK are expected to have a meaningful acceleration in real income growth — to around 2% by end-2024 — as the gas shock following Russia’s invasion of Ukraine fades.

- Rate hikes and fiscal policy will continue to weigh on growth across the G10 economies, but the worst of that drag has already happened, Hatzius writes. The team’s research shows that the maximum impact of monetary tightening on the growth rate (as opposed to level) of GDP occurs with a short lag of about two quarters. “We therefore expect a smaller drag from tighter financial conditions in 2024 than in 2023, even after factoring in the recent increase in long-term interest rates,” Hatzius writes.

- Industrial activity has been weak amid a rebalancing of spending back towards services from goods, the European energy crisis, an inventory cycle that had to correct for overbuilding in 2022, and a weaker-than-expected rebound in Chinese manufacturing. Most of these headwinds are forecast to fade this year, and manufacturing is expected to recover toward longer-term trend levels.

- The “most novel reason” to be optimistic about GDP growth is that central banks don’t need a recession to bring inflation down, and will therefore try hard to avoid one, Hatzius writes. Our economists’ analysis of past hiking cycles shows that major central banks are twice as likely to cut rates when there’s a risk to growth once inflation has normalized to sub-3% rates (relative to when inflation is above 5%).

Will central banks cut interest rates next year?

Policymakers in developed markets are unlikely to cut interest rates before the second half of 2024 unless economic growth proves weaker than anticipated, according to Goldman Sachs Research. In part, that view is based on our economists’ baseline forecasts, which expect inflation to remain modestly above target, unemployment rates to stay below their long-run levels, and GDP to grow roughly at trend pace in 2024. In emerging markets, policy cuts are expected to be announced sooner.

Japan stands apart because its inflation pickup was largely desired. After three decades of anemic price pressures or outright deflation, wage increases in 2023 signalled that the Bank of Japan was moving towards its goal of establishing a virtuous cycle between wages and prices.

The BoJ is therefore poised to move toward an exit from its policy of yield curve control in April 2024, although a formal abandonment of these measures is unlikely until October 2024, according to Goldman Sachs Research. Even so, Japanese inflation should remain far below the levels experienced by its G10 peers during this cycle.

China also stands apart when it comes to policy stimulus, as authorities have sought to counteract sluggish economic growth. Our economists expect China’s GDP growth to slow to 4.8% in 2024 as the boost from post-covid reopening fades, but partly offset by a slightly smaller housing drag, a modest rebound in global trade, and additional policy easing.

The world’s second-largest economy still has challenges, however. Its property downturn is likely to endure, and there is still a risk that the resulting pessimism becomes entrenched. The country’s ongoing demographic deterioration and persistently shrinking working-age population will require it to reinvent its growth model. A modest cyclical rebound in exports is unlikely to reverse the ongoing diversification of global value chains away from China. “Near-term growth in China should benefit from further policy stimulus, but China’s multi-year slowdown will likely continue,” Hatzius writes.

This article is being provided for educational purposes only. The information contained in this article does not constitute a recommendation from any Goldman Sachs entity to the recipient, and Goldman Sachs is not providing any financial, economic, legal, investment, accounting, or tax advice through this article or to its recipient. Neither Goldman Sachs nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the statements or any information contained in this article and any liability therefore (including in respect of direct, indirect, or consequential loss or damage) is expressly disclaimed.