Joshua Lu, co-leader of the Asia Consumer Research business unit in Goldman Sachs Research, discusses how India’s young population, improved education and growing economy are creating a vast new consumer market driven by mobility and connectivity.

Read the new Goldman Sachs Research report excerpt: India Consumer Close-up: Tapping the spending power of a young, connected Urban Mass

READ REPORT [22 pages, 2 MB]

India’s rapid growth is creating a new generation of consumers that promises to be an increasingly important market for years to come. In an excerpt from a new report, India Consumer Close-Up: Tapping the spending power of a young, connected Urban Mass, Goldman Sachs Research analysts explore how the sheer size of India’s youth, combined with improved education and a growing economy, is opening up unique opportunities to reach an emerging class of tech-savvy, well-educated urban consumers.

TOP TAKEAWAYS FROM THE REPORT

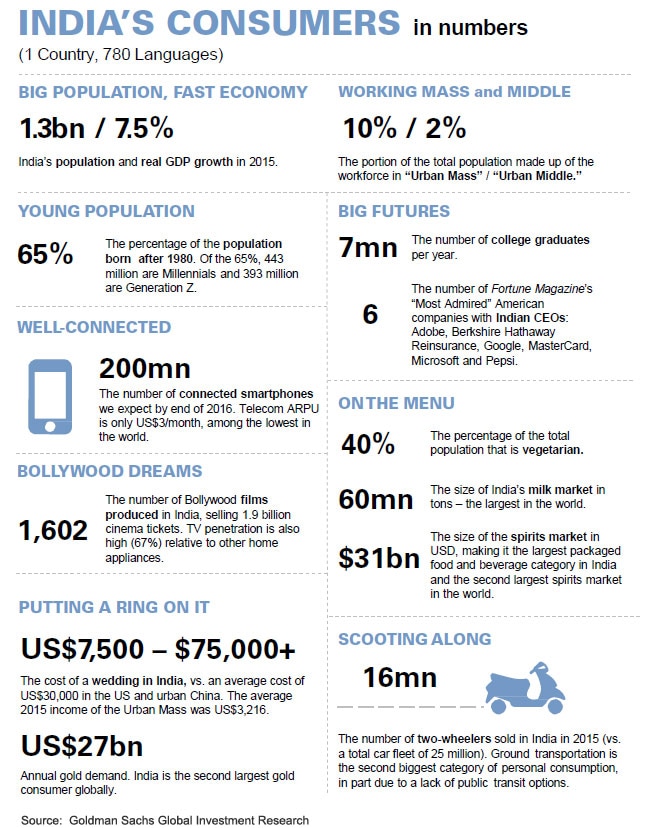

1) India’s consumer story will be shaped by its 440mn Millennials and 390mn Gen Z (born after 2000). The sheer size of India’s youth combined with improved education pave the way for sustained growth in purchasing power and makes India’s consumer story one of the world’s most compelling for the next 20 years. The nation’s challenge is to create enough jobs to unleash the productivity of India’s talented youth.

2) India’s GDP per capita– at US$1,650 in 2015 – is comparable to China in 2005. In the coming decade, India’s consumer story will be led by its 129mn Urban Mass consumers. This marks a different path from China, which was predominantly an Urban Middle formation story during 2002-2012.

3) India’s Urban Middle cohort is relatively small. We estimate that the workforce that falls into the Urban Middle (over US$11,000 annual income) stands at 27mn, or 2% of population.

4) Brand investing will be a big theme in everything. But we note: India’s Urban Mass will trade up into brands that offer the most incremental value and quality, but may not readily jump to aspirational brands. In purchasing a car for example, for an Indian consumer, an important input is the brand’s reputation for fuel efficiency.

5) Best categories positioned for profit pool expansion: packaged snacks, baby products, premium personal care, scooters, SUVs and jewelry. But one profit pool may grow faster than them all: restaurants.

6) Where India will leapfrog the most: Mobile connectivity and Ecommerce. Payment system and supply chain challenges remain but are not insurmountable. Improved mobile connectivity will also challenge the domination of TV as a primary source of household entertainment over time, creating a bigger profit pool for content providers and mobile gaming.

7) Growth of luxury and high end in general will be limited. Culturally, India’s affluent consumers tend to shy away from ostentatious display of wealth. One area where Indians do splurge: weddings. The number of weddings and household formations will increase over the next 5 years, given India’s demographics (peak birth numbers reached 22-23 years ago).

INDIA'S CONSUMERS IN NUMBERS