Since the Bank of Japan (BoJ) surprised markets in January with the introduction of a negative interest rate, the Swedish Riksbank and most recently the European Central Bank (ECB) have lowered their rates for excess liquidity absorption further into negative territory. In total, five central banks now “charge” financial institutions to store excess reserves—though the motivation for venturing below zero and the reserves subject to negative rates vary by bank.

To help make sense of negative rates and how they’re applied, Goldman Sachs Research has updated the “Top of Mind” primer published on the topic last year.

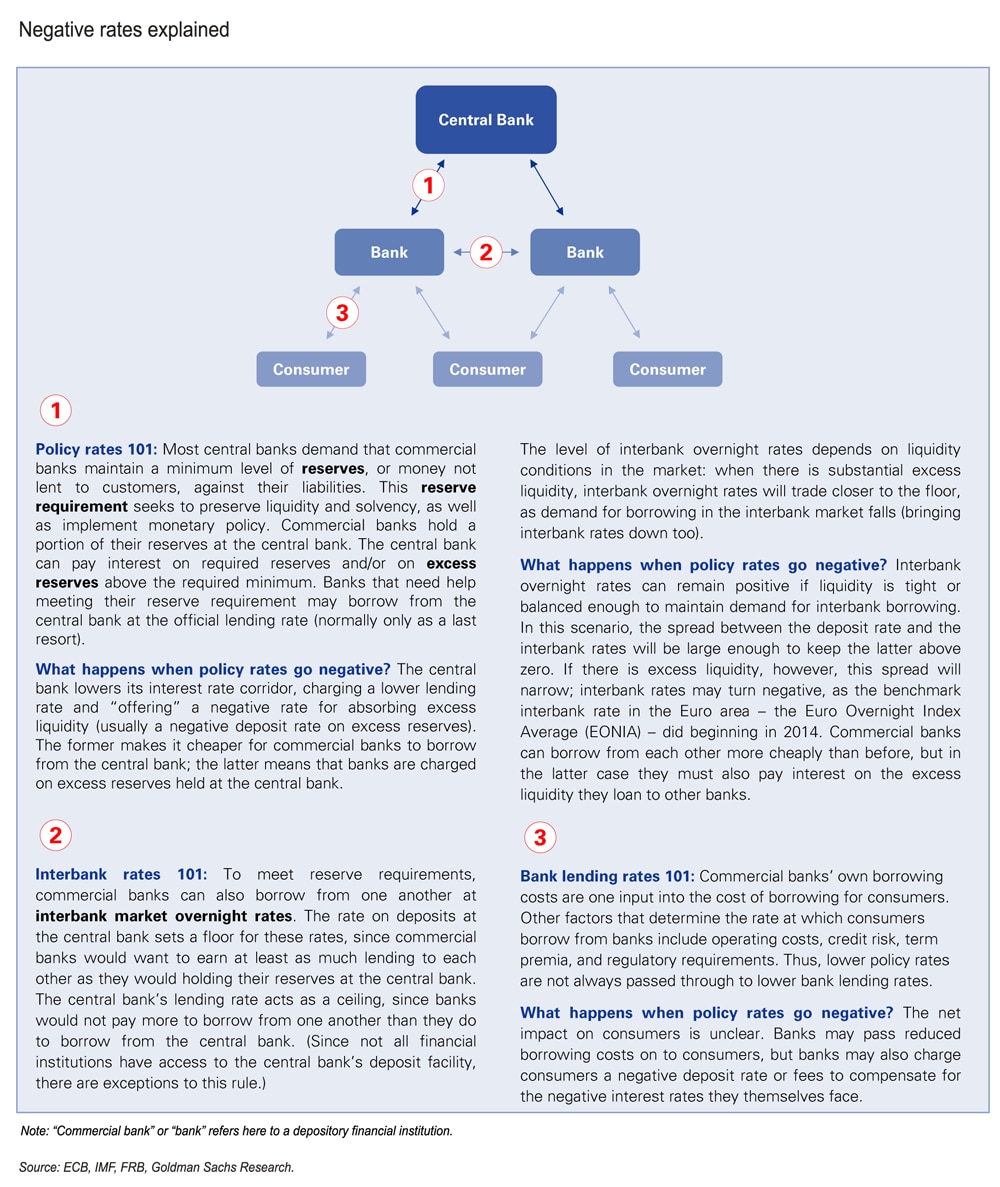

The many different rates (and what happens when one goes negative)

The following graphic explains the relationships between different types of interest rates and the impact of a negative policy rate.

Which central banks use negative interest rates?

Currently, five central banks “charge” financial institutions a negative interest rate for excess liquidity absorption. The motivation, magnitude and balance subject to negative rates varies by bank.

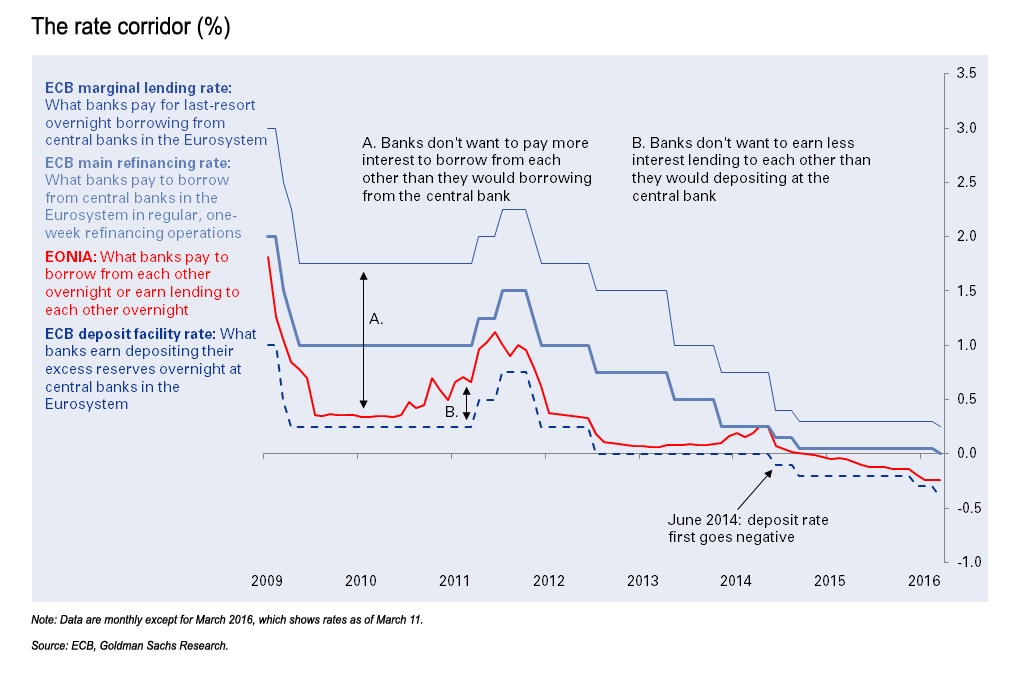

The ECB Experience

Despite speculation that the ECB would adopt a tiered-rate system for central bank deposits, the bank maintained its one-rate-fits-all-excess-reserves structure at the March meeting. As of March 16, financial institutions will pay a premium equivalent to 0.4% of their excess reserves (up from 0.3%) when depositing overnight at central banks in the Eurosystem. The graphic below shows this negative rate (the deposit facility rate) in relation to the main refinancing rate, lending rate and interbank rate.

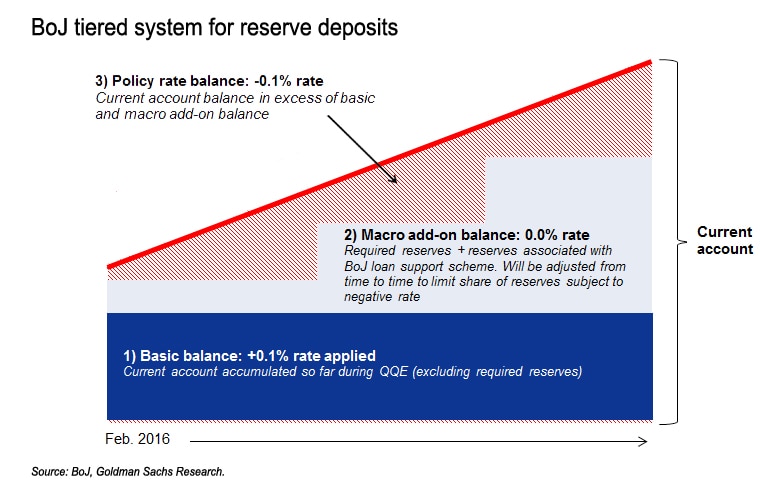

The BoJ Experience

The BoJ surprised markets in January 2016 by introducing a negative interest rate (-0.1%) for banks’ current account balances at the BoJ. Though not the first to go negative or the first to tier rates, the BoJ is the first central bank to use a three-tier structure, applying a different interest rate to different portions of each financial institution’s outstanding balance. The BoJ divides up current accounts as follows:

1. Basic balance (rate: +0.1%): The average of all BoJ current accounts outstanding in 2015 (including funds accumulated under quantitative and qualitative easing, or “QQE”), minus required reserves. The BoJ will continue to apply a positive interest rate to the basic balance to prevent pressure on individual bank earnings.

2. Macro add-on balance (rate: 0.0%): The balance made up of:

- Reserves financial institutions deposit with the BoJ to satisfy reserve requirements;

- Reserves associated with the BoJ's lending support programs;

- The product of a multiplier applied to the basic balance. The multiplier is currently zero, but the BoJ plans to adjust it from time to time to control the size of the macro add-on balance (and thus the portion of the current account subject to a negative interest rate).

3. Policy rate balance (rate: -0.1%): Any deposits a financial institution stores at the BoJ in excess of #1 and #2.

Put more simply, financial institutions that have excess reserves at the BoJ (greater than the basic balance and macro add-on balance) will pay a premium to continue storing these funds. To keep the size of the policy rate balance in check as QQE proceeds, the BoJ will increase its multiplier so that the macro add-on balance expands instead.